Convertible Bond Fund Not All It’s Cracked Up to Be

The AllianzGI Convertible Fund is touted by fund managers as producing better returns than stocks while having less risk. Don’t believe everything fund managers tell you.

In spite of investors thinking that corporate bonds are generic, they do come in several different flavors, including convertible bonds. Convertible bonds are called that because they start out as a bond and can later be converted to equity in the company, otherwise known as stock.

Companies issue convertible bonds at times where they want to raise more money but may not want to do it by issuing new shares. New stock issuance not only dilutes the value of existing shares, they also carry with it a negative perception by the market, where they may trade in an additional discount, in other words, value the stock lower than the net effect of the dilution.

Convertible bonds take a sneakier approach to this in a way, where the equity that gets added this way is less transparent and while any increase in the amount of shares out there, including other tricks such as options and warrants, all involve proportionate dilutions, these tactics have these additions more whispered and therefore don’t invoke the ire of the stock market in the same way.

There are other reasons why companies may wish to issue these convertible bonds, but nothing that really invokes the interest of investors, although the seeking to expand the market for their marketable securities beyond the normal vanilla stocks and bonds that people confine just about all of their investing to does provide additional opportunities, at least if you play a tune that they want to hear.

There are plenty of folks who have a natural preference toward bonds, thinking that stocks are a little too risky for their tastes. Buying bonds that can be converted into stocks is a concept that may serve to bridge the gap with stocks that these investors may struggle with a little. Even though people invest in convertible bonds through funds which assigns these decisions to them, decisions on converting the bonds to stocks, this can certainly serve to get them more comfortable with convertible bonds, especially with the right sales pitch.

The pitch with these is that they allegedly provide investors with similar returns to stocks with considerably less risk. If this is actually true, this may be a good reason to invest in a convertible bond fund such as the AllianzGI Convertible Fund, a top fund in this category, and in fact it would be a mistake to invest in stocks straight up when you can achieve the same returns than with stocks that this fund boasts with less risk.

Beating the stock market over the last 25 years is a big enough achievement, something that very few fund managers can claim, but when you do this with less volatility than the stock market, that makes the achievement even more noteworthy and is indeed something to be proud of. AllianzGI Convertible Fund managers Justin Kass and Doug Forsyth stand proudly behind this 25-year record, with the media raising the arms of these gentleman in the air in victory.

To hear this story told in the popular financial media, the performance of this fund as portrayed looks like quite an achievement indeed, and may even serve to attract not only more bond investors but even convince some to come over from the stock side of things. Few investors go all in with stocks and usually mix in a good amount of bonds into their portfolio, and if these convertible bonds are better than both stocks and bonds, they sure look like a good place to have some of your money.

From our perspective, while we really like better performance, and don’t consider the returns of the S&P 500 to be all that attractive, we don’t just stop at the hype, and we all need to be willing to go deeper than just hearing that a fund beat the S&P 500 over the last 25 years and had a lower beta.

It is not that there are just two choices here, this fund or the S&P 500, which you can trade these days with the SPY ETF that mirrors its movement, as we can’t just stop there and need to look at what else we could invest in instead, like for instance the Nasdaq 100 tradable through the QQQ ETF.

While we realize that only a small percentage of investors will want to do their own stock picking and put together stock portfolios on their own, which can significantly beat all the indexes when done right, we realize that investors generally want to go with an index instead and also prefer a broader index rather than sector indexes, as even sector indexes require management, to be in the right sector at the right time.

Many investors just want to plop their money down on one thing, like one of these index ETFs, and then watch it grow, which may not be ideal but is fine and has worked out pretty good over the years. If convertible bonds is really competitive with these index ETFs, especially the QQQ which has been clearly the better of the two for a long time now, then we will be suitably impressed, although we will need to go into the matter a little more deeply than just comparing this fund to the SPY over just a 25-year period.

Just being given these 25-year results by the fund managers, without looking at anything else, is a big red flag for us, and even if we did not know anything about this sort of investment beyond what they are telling us, we’d be quite skeptical about how this has gone in more recent times, times that matter considerably more than the very long view that they are trumpeting.

The 25-year numbers that they provide are truthful, as their fund did beat the S&P 500 over this time, albeit by a very small amount, and was slightly less volatile, with a beta of 0.98 since inception in 1993. SPY has a beta of 1 and it’s the benchmark for this, so this means that this convertible bond fund was less volatile although not meaningfully so over this time.

A beat is still a beat though, no matter how small, but we still need to account for the magnitude of these changes to want to switch to something, where we may insist on more substantial differences to be willing to do this. The allure of this being related to bonds is what is being counted on here, as without that, based upon the data they provide, these investments would be very substantially similar and would not represent much of a reason to make the switch.

We Can’t Invest Well If We Don’t Understand Risk Well

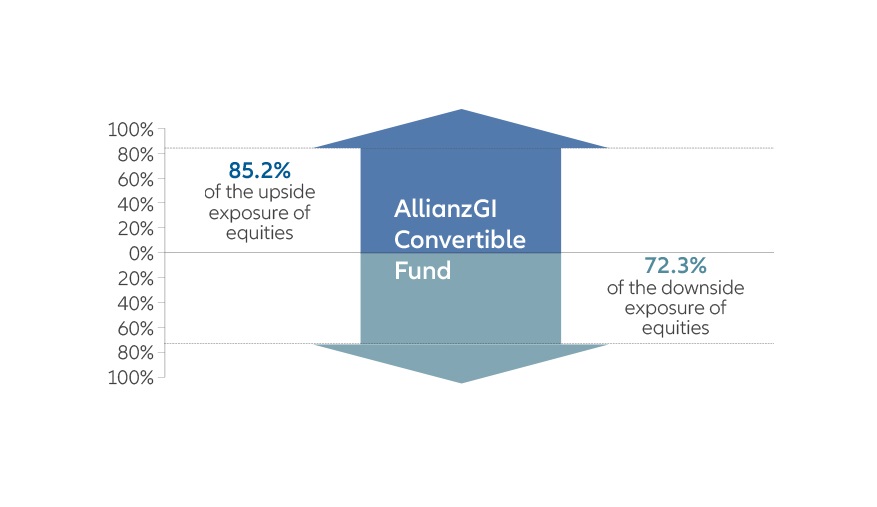

According to Kass, “an ideal convertible should have 60% to 80% of the upside of the underlying equity and 50% or less of its downside.” If that is what he is shooting for, this is a clearly inferior risk to return ratio to stocks overall even if this ideal is achieved, even though the perception of investors may find such a thing quite favorable.

Concerns about volatility tend to be grossly overstated by investors, and while there are times where we do need to be more concerned about volatility risk, with amounts that we have a short window with, this is not so much the case generally. The concept of discounting volatility over time is central to the buy and hold strategy that so many investors subscribe to, where if you take a long enough view, we can even ignore temporary drawdowns, even the bigger ones such as we saw in 2008, and instead focus our attention on where we end up, the returns part of it.

If someone was already in retirement, then cutting their drawdown risk by half while achieving 60-80% of stock market returns may seem pretty appealing indeed, even though this presumes that investing with this lower drawdown risk is the only way to manage this. We could just sell in times of trouble, like we could and should have done last February when the risk of stocks declining went through the roof, but among those investors who can never bring themselves to do the right thing even with a gun pointed at their heads, this strategy may have its time and place.

It doesn’t have its time and place all the time though, as over longer periods, the longer time horizons that the majority of investors can take advantage of, the time between now and when you need to spend at least half of your money as the typical benchmark for calculating this, even this less drawdown isn’t going to mean very much and the price of seeing your returns diminished by 20-40% isn’t even close to being worth it.

In both scenarios that are assumed here, we’re holding these investments regardless of what happens, and if we do this over the long run and end up well short of where we would have been if we invested in a stock ETF instead, it should be of no consolation that the stock ETF dropped more over this time given that this had no effect on our actual results.

We need to go beyond his ideal though and look at what has actually happened, and if drawdown risk has only been reduced by 0.02 during the last 25 years, that’s simply not meaningful. 25 years is a long time though and we need to look at more recent performance to get a better handle of how this convertible bond fund has done in more recent times, and it turns out that there are some very good reasons why you don’t see the fund tout these more recent results.

Mutual funds don’t have charts to look at, but ETFs do, and it turns out that this fund has been offered as an ETF since 2010, and we have 10 years of charting to look at. There’s something to be said about the visual experience of looking at charts, and this one looks very ugly as it turns out.

Even though higher risk and volatility doesn’t necessarily represent that much of a concern, and is once again more of a situational thing, if you have too much of this sort of thing, that can make exiting when you need to a lot trickier and riskier. When you see this alongside a fund that’s touted to be considerably less volatile though, if the thing turns out to be considerably more volatile than the S&P 500 instead, we at least need to clear up this confusion, or in this case, this distortion.

We can start with the beta of the fund, and compare it to both SPY and QQQ over the last 10 years to see how they stack up. SPY always has a beta of 1.0, and has delivered an average return of 13.04% over these last 10 years. QQQ has a beta of 1.05 over the last 10 years, and over the last 3, their beta has dropped to 1.01%, virtually identical to SPY, but with an average return of 18.96% over the last 10 years.

Our convertible bond fund has had a beta of 1.25 over these 10 years, which has been very consistent over this time, with the 5-year beta coming in at 1.22 and its 3-year beta at 1.24. To put this beta in perspective, high flying Apple, particularly known for its volatility, has a beta of 1.17, although this higher volatility is more than offset by its average total return of 116%, including dividends, over the last 10 years.

Things Are Not Always as They Appear

These results tell a very different story than the one told by the firm, and while this convertible bond fund has achieved the goal of the 60-80% return of stocks against SPY at least, with their 11.04% representing 85% of the return of SPY, this has only provided 58% of the return of QQQ, almost cutting the return in half while being much more volatile.

We end up in a place that actually is quite amusing, where investors would be quite eager to put a lot of money in this convertible bond fund over SPY, from believing the fable that it is less risky. They certainly would think that QQQ is a lot riskier, even though it’s actually a lot less risky, and certainly would think that putting all their money in Apple would be hideously riskier than the bond fund, when the truth is that the bond fund is the riskier of the two by a good margin, with less than 12% of its return.

The course that Apple has taken over the last 10 years has been to climb very high on the mountain with a few steps back along the way. Each time it has stepped back, it ended up higher on the mountain than before it, on an upward path.

It is well worth taking a moment to compare the paths that both Apple and this bond fund have taken over this time to get a better sense of how being more volatile isn’t a bad thing, but only if we get rewarded enough for it.

Apple has had 4 major pullbacks over this time. It started out its 10-year journey at $35, and it’s first pullback in 2012 saw them fall from $100 to $60, a big move indeed, but this stock does go down more than the market to be sure. If you bought it in 2010 and had the misfortune of selling at this bottom, at $60, that would still give you a 71% return over 2 years, way better than either stock indexes or bond funds of any sort.

The next dip was in 2015, where Apple fell from $132 to $90, another full-sized bear move, but with a considerably higher low. The 2018 bear move that hit the market saw another big drop with Apple, from $227 to $150, but once again, we’re left a lot higher. 2020’s coronavirus selloff saw Apple tank as well, from $324 to $229, although it has more than recovered and is up to $364 these days.

When you start at $35 and grow to $364, and were planning on holding it over this time, you should not even care about the fact it dropped considerably more than the market during leaner times, when the worst of this has you still crushing market returns. Higher beta can be a concern with underperforming investments such as this bond fund, but if an investment’s performance advantage is sufficient, this can totally negate these concerns and then some, as we can clearly see.

We see the same thing with QQQ although on a much more modest scale. We started at $42 10 years ago, and didn’t get a major pullback until the bear market of 2018, where it fell from $185 to $147. $147 is a much bigger number than $45 of course, meaning that this ETF had built up so much of an advantage over this time that a little extra drawdown here versus SPY that we sometimes see still left them well ahead even at the worst of it.

The same was the case with QQQ’s 2020 plunge, from $230 to $170, and this $60 drop was more than offset by the gains since the last one. This is the part that just about everyone misses, the fact that we should not worry about a bigger move down when it is proceeded by a much bigger move up to offset it and a lot more.

QQQ is now back up to $246, recapturing everything that was lost and adding another $16 per share to the previous all-time we fell from for good measure. This extra 0.05 of beta over the last 10 years has paid handsomely, nowhere near as handsome as Apple has been, but if we just look at the amount of drawdown and not look at the corresponding upside, we can be left pretty deluded and afraid of things we should not be afraid of.

In comparison, the path our convertible bond fund has taken hasn’t been very impressive, and well demonstrates when high beta actually does become a concern, when the swings downward are large but are not offset very much by accumulating returns.

Their ETF opened up at around $28 in April of 2010. 2011 saw the fund rise to $31, then drop later in the year all the way down to $26, below its issue price. It rose to $37 in 2015, but by 2016, it had fallen back to $26 again.

In late 2017, it rose back up to $35, just to see it dip down to $28 in early 2018. By the fall of the same year, we had our first legitimate bear market with stocks over these 10 years, seeing this convertible bond fund fall from $32 to an all-time low of $24, a 33% decline compared to the 20% that SPY and QQQ gave back.

2020 saw this fund do the $32 to $24 dance again, when this fund marked its 10-year anniversary and got to celebrate that with a price even lower than when they started a decade ago. Like just about everything else, it has recovered since, but the $33 that it trades at now is not much further up on the mountain than the $28 it started at over 10 years ago now.

This does pay higher dividends than average, but that only goes so far, and nowhere near enough to make this investment competitive. When you both end up with these big drawdowns and what turn out to be clearly inferior total returns when everything is calculated in, this makes for a very ugly investment indeed.

This is the side of the fund that the fund managers certainly don’t want you to see, showing you a piece of their lawn that is nice and green while the lawn behind the curtain is a lot browner than anyone should want. As long as you don’t peek behind the curtain, you can certainly be duped into thinking that this fund is at least a comparable investment to stocks.

It takes so little to expose these facades when they exist, and all we’ve done is pull back the curtain for you a little here but that has been more than enough to give us the much better perspective that we need to decide whether we want to put our money on this broken down horse.

The bigger lesson here has been to not just look at beta in isolation and let that scare us, and having higher betas scare investors much more than they should is at epidemic levels. There are times where we should be scared of higher betas though, when their performance does not justify it, and especially when they underperform this much.

It is wise to be afraid though in some cases though, and the AllianzGI Convertible Fund stands as a fine example of not what we should want, as the fund managers and some financial media writers wish us to believe, but a fine example of what we should not want, once we open our eyes enough.

Chief Editor, MarketReview.com

Ken has a way of making even the most complex of ideas in finance simple enough to understand by all and looks to take every topic to a higher level.

Contact Ken: ken@marketreview.com

Areas of interest: News & updates from the Federal Reserve System, Investing, Commodities, Exchange Traded Funds & more.